📋 GHG Protocol Is Rewriting the Scope 3 Rules.

The proposed updates to the world’s most-used value chain emissions standard will change how companies calculate, verify, and report their biggest carbon numbers.

The GHG Protocol has published a Phase 1 Progress Update on the revision of its Corporate Value Chain (Scope 3) Accounting and Reporting Standard, the global benchmark for measuring supply chain and product-lifecycle emissions. The proposals are not final, but they signal a material shift in what “complete” and “credible” Scope 3 disclosure will mean. If your emissions reduction targets, customer reporting, or product-level claims rely on Scope 3, these changes affect your methodology, your data infrastructure, and potentially your numbers.

🔍 Why now

The original Scope 3 Standard was published in 2011 (Source: GHG Protocol). Since then, it has been adopted by virtually every major sustainability framework: the IFRS Foundation’s ISSB standards, the European Sustainability Reporting Standards (ESRS) underpinning the EU’s Corporate Sustainability Reporting Directive (CSRD), and SBTi’s target-setting methodology. The standard hasn’t kept pace with the ambition placed on it.

Three forces are driving this revision now. First, regulatory mandates like CSRD and SB 253 have dramatically expanded the population of companies required to report Scope 3, exposing inconsistencies in how companies apply the existing categories. Second, data quality across value chains has improved enough that the standard’s current vagueness on inputs is no longer justified. Third, new business models — licensing, facilitated finance, platform transactions — have created categories of value chain emissions the 2011 standard simply never contemplated.

The revision is being developed by Technical Working Groups. A complete draft standard for public consultation is expected, though no final publication date has been confirmed (unconfirmed — verify before planning).

🎯 Who is in scope

The Scope 3 Standard applies to any company using GHG Protocol’s Corporate Value Chain framework, which includes:

Directly affected: Companies reporting under CSRD (ESRS E1), SB 253, ISSB S2, and any voluntary framework that references GHG Protocol methodology. This covers a wide cross-section: large EU-based companies already in scope for CSRD, California reporters with $1B+ revenue (Source: SB 253), and companies submitting SBTi-validated targets.

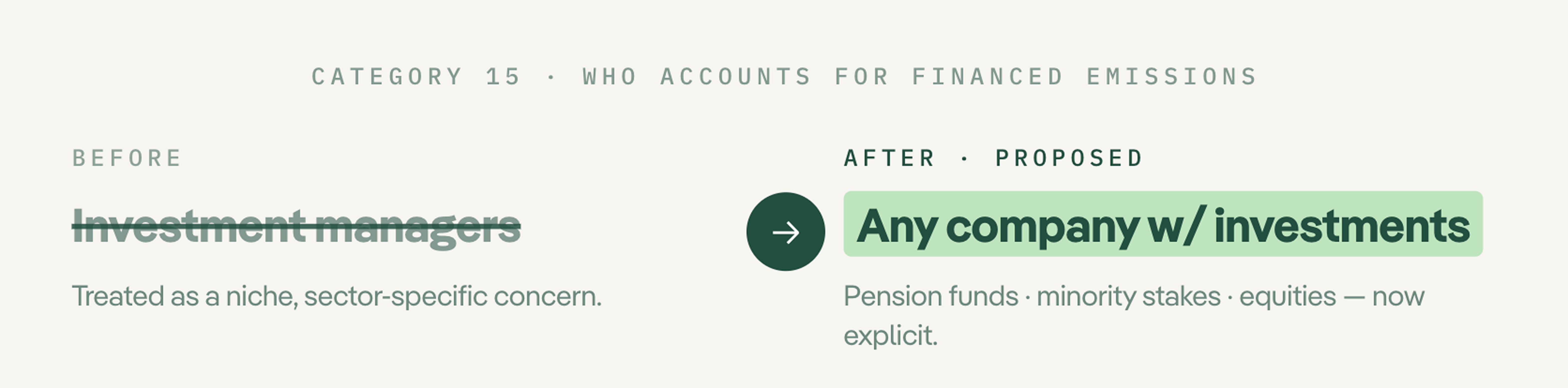

Financial sector: Proposed changes to Category 15 (Investments) clarify that the category applies to all companies, not just investment managers. Any company with a sizeable investment portfolio needs to track this closely.

Indirectly affected: Any company that sells to CSRD-covered customers will face upstream pressure. Customers required to report Category 1 (Purchased Goods and Services) emissions will demand better primary data from their suppliers — which is where most of the data quality burden lands.

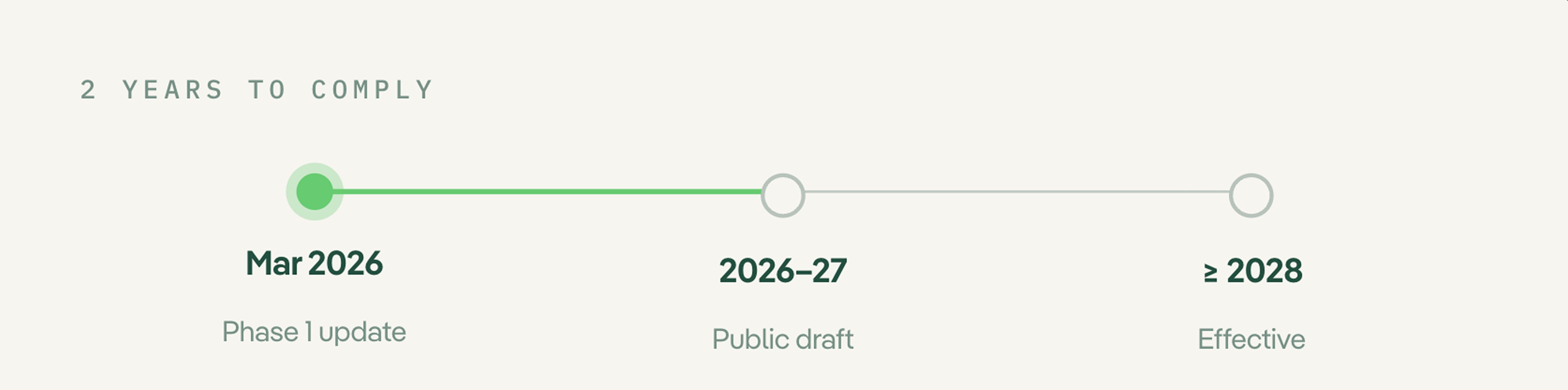

📅 Timeline

The revision process is underway but the final publication date is not confirmed. Based on GHG Protocol’s stated process, the sequence currently looks like this:

The Phase 1 Progress Update was published in March 2026 (Source: GHG Protocol). A complete draft standard for public consultation is expected to follow, likely in 2026 or 2027 (unconfirmed, based on typical GHG Protocol consultation timelines — verify before planning). Final publication would follow a public comment period, placing the effective date likely no earlier than 2027–2028. No mandatory adoption transition period has been specified.

The timeline matters because companies that need to recalculate historical Scope 3 inventories under a revised standard will face restatement work that requires months of lead time, not weeks.

📊 What the key proposals actually change

1. The 95% coverage requirement

The current standard says companies “shall account for all Scope 3 emissions and disclose and justify any exclusions.” The proposed revision replaces that language with a concrete threshold: companies must report at least 95% of total required Scope 3 emissions to be in conformance (Source: GHG Protocol Phase 1 Progress Update, March 2026). The remaining 5% can be excluded, provided it covers only minor sources.

This is a harder test than it sounds. Many current Scope 3 inventories exclude categories that are difficult to measure, not necessarily minor. Under the proposed rule, you’d need to demonstrate, with data, that excluded categories fall below the 5% materiality threshold. That requires a rough estimate of what you’re not measuring, which itself requires data.

2. A new Category 16

The proposed Category 16 would capture “other value chain activities” including facilitated emissions (third-party activities generating emissions from which a company earns direct, transactional income, without owning or controlling the activity) and licensing-related emissions. Most Category 16 reporting would be optional under the current proposal (Source: GHG Protocol Phase 1 Progress Update, March 2026). This is most relevant to financial platforms, marketplaces, and IP-licensing businesses where current categories produce incomplete pictures.

3. Revised data quality and tiering requirements

Companies would be required to disaggregate reported Scope 3 emissions into distinct tiers by data type for each category: primary data, secondary data with supplier-specific inputs, industry averages, and so on. The intent is comparability. The operational consequence is a more granular data management requirement than most current Scope 3 programs maintain.

🧠 What this means strategically

For companies with validated SBTi targets, a methodology change in the underlying GHG Protocol standard could require recalculation and resubmission. The 95% coverage rule, in particular, may reveal that current inventories need to be extended before they qualify as conformant.

For companies subject to CSRD, ESRS E1 is built on GHG Protocol methodology. A revised Scope 3 Standard, once published, will likely propagate into CSRD guidance updates. Companies that built their CSRD data programs around current category definitions may face scope adjustments.

For suppliers to large enterprises: the data quality tiering requirement is where pressure will concentrate. Your customers will increasingly ask for primary data rather than industry averages, because their own conformance depends on the quality of what you supply. This is less a compliance question than a commercial positioning question for B2B companies.

💡 One thing most summaries miss

The proposal to clarify that Category 15 applies to all companies, not just investment managers, is being underreported. Companies with pension funds, minority stakes, or equity portfolios have often treated financed emissions as someone else’s problem. Under the proposed revision, they would need to account for them explicitly. The parallel proposal to reclassify insurance underwriting and certain financial services into optional Category 16 sub-categories partially offsets this, but the net effect is a broader scope for most non-financial companies with investment assets.

✅ What you should do now

Start by auditing your current Scope 3 inventory against the proposed 95% coverage threshold. For each excluded category, produce a rough estimate: if you cannot demonstrate it represents less than 5% of total emissions, it belongs in scope. That exercise will also tell you where your data gaps are most material.

Second, if your company operates financial services, a marketplace model, or licenses IP at scale, review whether the proposed Category 16 creates a new disclosure obligation or clarifies an existing one.

Third, if you have SBTi targets, contact your account team to understand how methodology updates will be handled during a standard transition period.

The data challenge across all three of these workstreams is the same: Scope 3 accuracy depends on supply chain data quality, and most companies don’t yet have the collection infrastructure to meet a tiered-disclosure requirement. If you’re building that infrastructure, Greenly can centralise supplier data collection and map it to GHG Protocol categories, rather than managing it across spreadsheets.

The full official GHG statement

👉 Want to stress-test your current Scope 3 coverage before the standard changes? Talk to Greenly